1911 Chinese £100 British Pound Imperial Chinese Government - Hukuang Railway Gold Bond (Uncanceled) - China Railway £100 British Pounds Gold Bond

Inv# FB5100 Bond

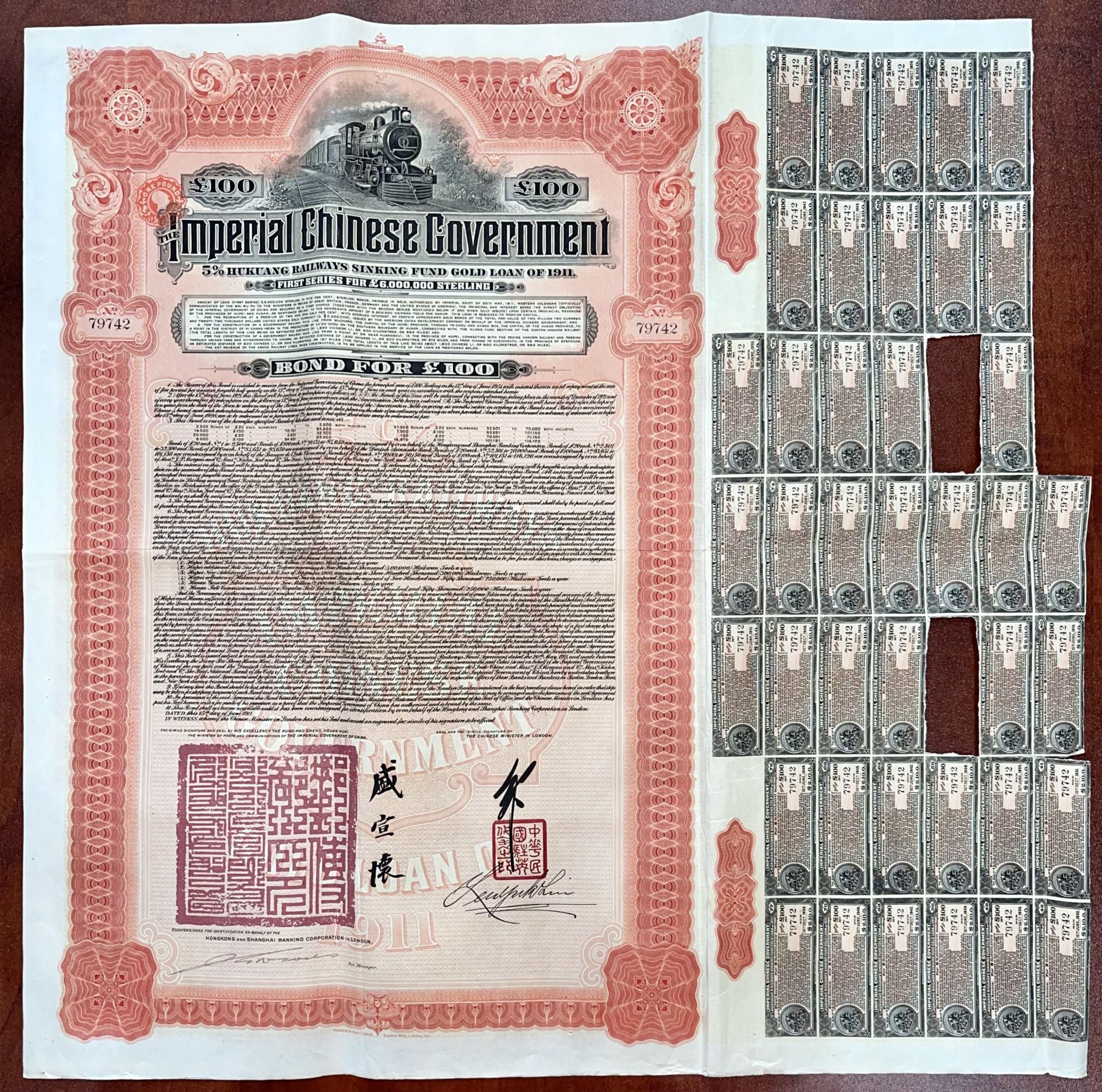

£100 5% Hukuang Railways Sinking Fund Gold Loan of 1911 Bond. Uncanceled. Several coupons. It is important to stress that these bonds have been bought in recent years and pretty much taken off the collector market. As a result prices have risen rather dramatically. Several more rows of coupons not shown. Extremely Fine Condition. Article relating to this Chinese item: https://www.bloomberg.com/news/articles/2019-08-29/trump-s-new-trade-war-weapon-might-just-be-antique-china-debt

Imperial Chinese Government Hukuang Railways bonds are well-nigh ubiquitous in the marketplace. They were issued in 1911 by a consortium of banks in London, Berlin, Paris and New York, with serial numbers running into the six digits, of which hundreds if not thousands appear to have survived. A few bear New York State adhesive revenue stamps; shown here is a New York issue £100 bond with Secured Debt $1 and Investments $1 stamps paying New York’s Investments tax in 1917 and 1918; this secured for the bondholder exemption from that state’s onerous personal property tax. Coupon bonds of this era are generally large and spectacular—American bonds typically measure about 10 by 15 inches—but this one sets new standards on both scores. It is huge, some 16 by 22 inches as shown. Its design and execution by security printers Waterlow & Sons of London are equally impressive, featuring the facsimile seals and signatures of China’s Minister of Posts and Communications and its Minister in Washington. Alongside is the countersignature of a representative of the New York banks J. P. Morgan & Co., Kuhn Loeb & Co., the First National Bank of the City of New York, and the National City Bank of New York. Beauty is in the eye of the beholder, and to my eye these Hukuang Railways bonds are among the most attractive pieces ever to bear stamps.

Similar bonds issued in London, Berlin and Paris by the Hong Kong and Shanghai Banking Corporation, Deutsch-Asiatische Bank, and Banque de L’Indo-Chine, respectively, show the signatures of their representatives and of the Chinese Ministers to Great Britain, Germany and France. Only the relatively few stamped bonds are philatelically interesting, but all are historically important. Surprising Historical Significance There is strong evidence that the controversial financing of the Hukuang Railway was the tipping point that sparked China’s revolution of 1911, which overthrew three millennia of dynastic rule and led to formation of the Chinese Republic the following year. No less qualified an observer than Sir John Newell Jordan, British Minister to Peking from 1906 until 1920, wrote with the benefit of hindsight at the end of his tenure that “the Hukuang Railway Agreement ... was the proximate cause of the downfall of the Dynasty.” (Woodhouse, 2004). The reader can be excused for finding it improbable that the terms of a railroad loan could trigger a revolution. The explanation is a tale worth telling. Invasion via Funding By 1911, nationalists had long protested the extent of foreign control of China’s railroads. As summarized by Goetzmann and Ukhov (2005), By most accounts the competition among the great powers to secure railway concessions during this period through a combination of political diplomacy and the financial might of their capital markets was, in some ways, the high point of the age of Imperialism. At least it was characterized as such by contemporary commentators such as Lenin, who used the division of China into spheres of influence by foreign capitalists as the example of Capitalist Imperialism par excellence. ... Virtually of China’s railways constructed after 1895 were financed by foreign debt issues underwritten by European-led investment banking syndicates which obtained right of way, property concessions and promises of repayment from the Chinese Imperial government. Under the control of the bankers who financed the loans, Chinese railways were constructed, owned and operated by managers designated by the financial consortium. Certainly the most contentious feature of these loans was their provision for extra-territorial rights by which foreigners enjoyed jurisdiction over portions of Chinese territory. The Chinese Eastern Railway was a prime example of extra-territoriality. The Russo-Chinese bank issued a 5 million tael loan in Russia in 1896 to finance the construction of a railway across Manchuria linking the Trans-Siberian Railway to Vladivostok. The railway and its right of way were entirely administered and policed by Russian officials, who controlled the receipts and disbursements. The line was, in effect, a little bit of Russian territory within China’s borders, and issued its own currency. Author’s note: To this it may be added that a contingent of Russian troops travelled on each train, housed at defense posts erected along the line; that the Chinese Eastern Railway had over 20,000 Russian employees; and that until the 1920s over 120,000 Russians lived in Manchuria, accounting for a quarter of its population, most dependent upon the C.E.R. for their livelihood.

The Hukuang Railways £6 million loan was the last in a long succession of foreign loans to the Imperial Chinese Government for railroad construction. No fewer than 27 such loans appear in the extensive list of Chinese external debt issues after 1861 compiled by Goetzmann and Ukhov (2005); the Hukuang loan was the largest, but three others were for amounts between $19.6 million and $22.5 million, and six more ranged from $6.5 million to $14.8 million. Just as numerous if somewhat less costly were 22 loans for war or defense, notably including a $6.5 million bond issue in 1885 to finance China’s defense against France during the 1880s. By far the largest obligations, though, were bonds to cover war indemnities imposed after China’s defeats in the 1894-5 Sino-Japanese War and the 1898-1901 Boxer Rebellion, amounting to some $100 million and $300 million, respectively. Crippling Guarantees Loans to the Imperial Chinese Government would not have been attractive to investors without strong guarantees. As security for its many foreign loans, the Manchu government pledged the proceeds of a vast array of revenues and taxes, so that by the time of its collapse nearly its entire revenue stream had been diverted to foreign banks. The most lucrative and dependable source of security was China’s considerable maritime customs revenue. This began to be attached beginning in 1866, and remained the preferred security for decades; it was the sole source of the massive war indemnities of 1895–1901, by which time virtually all maritime customs revenue was pledged to service foreign debt. New sources of security now had to be found, and subsequent foreign loans tapped the proceeds of various domestic taxes, most often salt and rice taxes and the “lekin,” a tax on internal transit of goods. With each loan the government incrementally lost control of its own finances. Hukuang Railway: A New Beginning Construction of the Hukuang railway was expected to break this mold. Hukuang (“lake plain”) is a region in south-central China including the provinces of Hunan, Hupei, and portions of Szechuan. The Hukuang Railway was to have two branches: one from Hankow south to the port of Canton, the other from Hankow west to Chengtu in Szechwan. Construction rights for the Canton-Hankow branch had been awarded to J. P. Morgan’s American China Development Company, but beginning in 1903 events took a radically different turn. The “Railway Regulations” of the Qing Government enacted that year granted domestic companies the right to operate railroads, and in 1904 the Ministry of Commerce promulgated reforms designed to facilitate development of domestic corporations. In 1905, with the active encouragement of the provincial governor of Hunan and Hupei, a consortium of Hukuang gentry, officials and businessmen first lobbied successfully for compensated cancellation of the construction rights of the American China Development Co., then obtained contracts to build the road. The Kwangtung Company of the Canton-Hankow Railway had an auspicious beginning; its entire capitalization of 44 million taels (some $60 million) was subscribed by Chinese investors rich and poor, making it the most successfully capitalized of all Chinese companies, by a very large margin. Most of the funds came from wealthy Chinese living abroad, but there was enthusiastic support from the populace as well. Shares were initially priced at only a single tael, and the North China Herald reported that Not only are the monied classes rushing to buy shares, but the poorest of the poor and even those who are supposed of no cash to spare and hardly enough to keep body and soul together are buying up one or more shares (Lee, 1977). The contract for the Hankow-Chengtu branch was entrusted to the Hupeh Company of the Szechuan-Hankow Railway.

The New Beginning Gone Awry and Undone The Kwangtung Company, though, was plagued by mismanagement and massive embezzlement. Its sister company, the Hupeh Company, raised only about 3% of its projected capitalization of 20 million taels. Years passed with no tracks laid or rolling stock purchased, and on May 9, 1911, the Qing government, bowing to diplomatic and political pressure, summarily nationalized all domestic railway development, and on May 20 re-awarded the contract to the aforementioned consortium of banks in London, Berlin, Paris and New York, which sponsored a £6 million bond issue to finance construction. The Imperial Government pledged as security the revenues of the railroad and the proceeds from six different taxes on salt, rice, and lekin, all of which are enumerated on the bonds themselves. Prelude to Revolution Until this point, opposition to foreign control of China’s railroads and mines had come from two sources with different aims and motives: a popular revolutionary movement, and the more organized “Rights Recovery Movement” promoted by gentry, merchants, landowners and officials. The revolutionaries wanted nothing less than the overthrow of the Manchu dynasty; to them the government’s surrender of rights to foreign governments and companies was just one of many objectionable policies. In contrast, the Rights Recovery Movement focused on foreign control of the mines and railroads, which it opposed primarily because it coveted that control for itself; it was essentially conservative and had no intention of overthrowing the Manchu government, on which it depended for the privileges it already enjoyed as well as those it hoped to gain. After the abrogation of their Hukuang Railway contracts, though, the infuriated gentry fomented anti-government protests in Szechuan. As summarized by Woodhouse (2004), The gentry-merchants power group demanded the cancellation of the Hukuang Loan contract. The provincial government supported this demand, for the provincial assembly was often made up of the local ruling class. The central government tried to pacify these groups without success. It proposed to exchange its railway shares for interest-earning government bonds, for the people in Hupeh and Hunan provinces. For the Szechuanese, however, it offered to redeem the sums spent solely for railway purposes rather than the sums actually subscribed. It was believed that such a policy was taken because Sheng Hsuan-huai had invested significantly in bonds in Hupeh and Hunan provinces but none in Szechuan province.

The outraged Szechuanese groups protested that the government intended to sell Szechuan to the foreigners... The local ruling class mobilized students, workers and peasants into their “patriotic” protest. On 5 August 1911 the Szechuanese banded together and convened the Defend Railways League, declaring their defiance of the Hukuang Railway Loan contract... By mid-September, the protest took the form of rioting and street fighting, and the revolt quickly spread throughout the province. Even so, the Szechuan uprising is not considered by historians to have been anti-dynastic in motive. The revolution is traditionally considered to have begun, not with the uprising in Szechuan, but with a coup at the Imperial Army garrison at Wuchang on October 10, 1911. The Revolution Begins by Accident Wuchang, directly across the Yangtze from Hankow, was the nearest garrison to Szechuan, and two regiments had been sent from there to suppress the uprising. In their absence, the revolution began by accident. The Hankow/Wuchang region was a hotbed of revolutionary activity, and with the garrison depleted, plans for an uprising were accelerated. A significant percentage of China’s New Army harbored revolutionary sentiments, especially at Wuchang, where potential rebels numbered an estimated one-fourth to one-third of the troops, and many had joined revolutionary secret societies. On October 9, 1911, a rebel bomb maker secreted within the Russian quarter at Hankow accidentally exploded one of his products. The ensuing police investigation uncovered a cache of incriminating evidence, and within hours three revolutionary leaders were arrested and executed. Among the materials found was a membership list of the Literary Society, whose innocent name belied subversive goals, which included soldiers at Wuchang. Alerted to their impending arrest and probable execution, they staged a successful coup the following day, taking the garrison and the city. The revolt spread rapidly; by October 16 the Prince Regent had proclaimed the abdication of the boy emperor from the throne, and within six weeks, fifteen provinces had seceded. Tilting at Windmills The government of the new Chinese Republic pledged in 1912 to honor the debts of its imperial predecessor, and a succession of subsequent governments made similar guarantees, with foreign loans always a high priority. In 1921 the Chinese government declared bankruptcy, and began defaulting on its loans, but interest on the Hukuang Railway bonds was paid until 1938, when Japanese invasion intervened. The government of the People’s Republic of China repudiated all such debts in 1949, but numerous lawsuits have been brought against it and the government of the Republic of China seeking redemption of various bonds. A quixotic 2005 judgment in a New York court, factoring in the stratospheric increase in the price of gold, placed the then-current value of a 1913 £100 gold bond at $27.75 million!

Mahler 2010

Goetzmann, William N., and Andrey Ukhov. 2001. China and the World Financial Markets 1870-1930: Modern Lessons From Historical Globalization. Wharton Financial Institutions Center working paper. http://fic.wharton.upenn.edu/fic/papers/01/0130.pdf accessed, 2010. Kahn, Helen D. 1968. The Great Game of Empire: Willard D. Straight and American Far Eastern Policy. Ph.D. Thesis, Cornell University. Lee, En-Han. 1977. China’s Quest for Railway Autonomy: 1904-1911. Singapore University Press, Singapore. Mahler, Michael. New York Mortgage Endorsement, Secured Debt, and Investments Stamp Taxes, 1911–20. http://www.revenuer.org/research_intro.htm accessed, 2010. Marvin L. Morris, Jr., vs. The People’s Republic of China and The Republic of China. United States District Court, Southern District of New York, filed May 6, 2005. http://www.globalsecuritieswatch.org/civil_complaint.pdf accessed, 2010. Woodhouse, Eiko. 2004. The Chinese Hsinhai Revolution: GE Morrison and Anglo-Japanese Relations, 1897-1920. London: Routledge.

A bond is a document of title for a loan. Bonds are issued, not only by businesses, but also by national, state or city governments, or other public bodies, or sometimes by individuals. Bonds are a loan to the company or other body. They are normally repayable within a stated period of time. Bonds earn interest at a fixed rate, which must usually be paid by the undertaking regardless of its financial results. A bondholder is a creditor of the undertaking.

Ebay ID: labarre_galleries