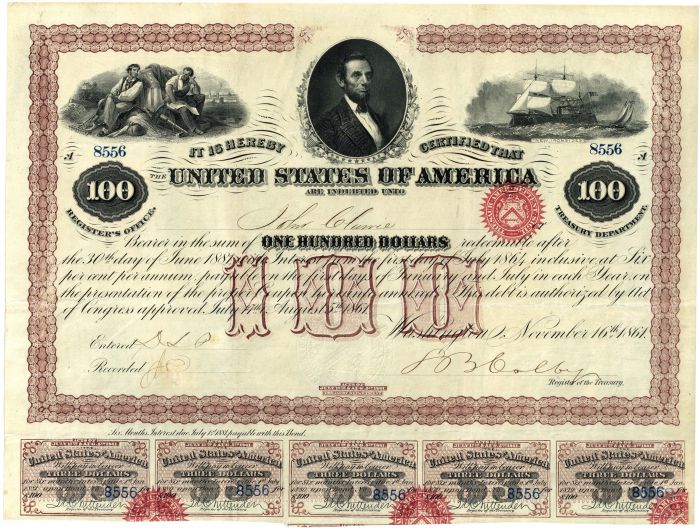

$100 United States of America Bond of 1861 - Only 2 or 3 known to Exist

Inv# TB1128 Bond

$100 United States of America Bond of 1861 - Only 2 or 3 known to Exist.

Signed by Stoddard Benham Colby (February 3, 1816 – September 21, 1867) was an American lawyer and political figure. He is notable for his service as Register of the United States Treasury during the American Civil War.

Colby was born in Derby, Vermont on February 3, 1816. He was educated in Derby, and prepared for college by studying in the office of attorney Timothy P. Redfield. He graduated from Dartmouth College in 1836, and was elected to Phi Beta Kappa. He studied law with William Upham, was admitted to the bar, and practiced law in Derby. In 1840 he was elected to a single term in the Vermont House of Representatives, and served from 1841 to 1843. In 1846 he began to practice in Montpelier as the partner of Lucius B. Peck.

He was an unsuccessful Democratic candidate for the United States House of Representatives in 1856.

Colby was appointed Register of the Treasury and assumed office on August 12, 1864.

He was married to Harriet Elizabeth Proctor, sister of Sen. Redfield Proctor. She was one of the victims of the Henry Clay (steamboat) disaster. They had 4 children.

Colby died in Haverhill, New Hampshire following a five-week illness. He was buried at Proctor Cemetery in Proctorsville, Vermont.

The Revenue Act of 1861, formally cited as Act of August 5, 1861, Chap. XLV, 12 Stat. 292, included the first U.S. Federal income tax statute (see Sec.49). The Act, motivated by the need to fund the Civil War, imposed an income tax to be "levied, collected, and paid, upon the annual income of every person residing in the United States, whether such income is derived from any kind of property, or from any profession, trade, employment, or vocation carried on in the United States or elsewhere, or from any other source whatever [ . . . .]" The tax imposed was a flat tax, with a rate of 3% on incomes above $800. The Revenue Act of 1861 was signed into law by Abraham Lincoln.

The income tax provision (Sections 49, 50 and 51) was repealed by the Revenue Act of 1862. (See Sec.89, which replaced the flat rate with a progressive scale of 3% on annual incomes beyond $600 (equivalent to $16,286 in 2021) and 5% on incomes above $10,000 (equivalent to $271,433 in 2021) or those living outside the U.S., and perhaps more significantly it was explicitly temporary, specifying termination of income tax in "the year eighteen hundred and sixty-six").

Prior to the Civil War, the United States faced a financial depression subsequent to the Panic of 1857, an event facilitated by over-expansion of the domestic economy and a European financial meltdown. In the three years preceding the Civil War, the Federal Government incurred a budget deficit exceeding $40 million. Coupled with the threat of secession, the Federal deficit placed the US government under considerable financial strain. In 1860, the US Treasury paid between 8 and 12 percent interest on government bonds in order to raise additional funds and meet public expenditures. In December 1861, the US Treasury attempted to sell five millions of interest-bearing notes at 12 percent but found itself able to dispose of only four millions. The Treasury's struggles illustrate the precarious nature of the US government's financial state. As the nation edged closer to war, the need to mobilize a volunteer force placed an additional financial burden upon the Federal government. While treasury notes with enticing interest rates allowed the US government to raise revenue quickly, they also established a need for additional revenue streams with which to pay off interest.

In March 1861, President Lincoln began to explore the federal government's ability to wage war against the South from a logistical standpoint. He sent letters to cabinet members including Edward Bates, Salmon Chase, and Gideon Welles inquiring whether the president had constitutional authority to collect duties ranging from an import tariff to a property tax. Documents housed at the Library of Congress indicate that Lincoln was concerned with the Federal government's ability to collect tariffs from ports along the Southeastern seaboard, noting the imminent threat of secession.

On July 4, 1861, President Lincoln opened a special session of Congress with the explicit purpose of addressing the Civil War from a legislative standpoint. One of the primary concerns facing Congress was the question of funding: given a surfeit of volunteers, the Union Army military incurred extraordinary expenditures as they trained and armed a martial force. President Lincoln noted that, "One of the greatest perplexities of the government, is to avoid receiving troops faster than it can provide for them. In a word, the people will save their government, if the government itself, will do its part" To raise revenue by approximately $50 million, legislators adopted a three-pronged approach consisting of an increase in certain import tariffs, a newly instituted property tax, and the first personal income tax.

Under the leadership of Senator William Pitt Fessenden of Maine, chair of the Senate Finance Committee, Congress drafted the Revenue Act of 1861 in a relatively short time-frame. While the legislation effectively introduced import tariffs, property taxes, and a flat rate income tax of 3% on those making above $800, it lacked a comprehensive enforcement mechanism. In Congress, the bill provoked considerable debate: Thaddeus Stevens, chairman of the House Committee of Ways and Means, declared that, "This bill is a most unpleasant one. But we perceive no way in which we can avoid it and sustain the government. The rebels, who are now destroying or attempting to destroy this Government, have thrust upon the country many disagreeable things." His sentiment reflected the view that the income and property taxes levied by the bill were necessary evils. The bill was eventually passed by Congress and signed into law by President Lincoln. Despite its sweeping reform, the ineffective enforcement mechanism coupled with a 3% flat tax rate failed to yield the desired revenue.

Tax structure

- Import Tariff: The Revenue Act of 1861 levied various tariffs on imports including sugar, tea, nuts, brimstone, coffee, liquor, and various fruits and herbs. The majority of imports were taxed on a per unit basis while certain imports, often those with more volatile pricing such as hides, citrus fruit, silk, and gunpowder were taxed ad valorem, with rates ranging from 10% on hides and rubber to 50% on wines. The act imposed an additional tax of 10% ad valorem on articles imported in foreign vessels from beyond the Cape of Good Hope. The provisions included in the act expanded upon the protectionist precedent set by the Morrill Tariff of 1861.

- Property Tax: The Revenue Act of 1861 instituted a tax on real estate, levied in proportion to each state's population. While the act's enforcement mechanism was limited, it formally established a system of tax districts, assessors, and collectors, laying the groundwork for the Internal Revenue Service's formation on July 1, 1862. The property tax drew criticism from representatives of rural states: by taxing real estate and excluding other forms of personal property, the tax, they argued placed an undue burden upon large, sparsely populated states and territories in the West and Southwest. Though densely populated states such as New York were assessed at a higher rate due to a large population, a greater proportion of wealth in such states was invested in personal property other than real estate.

- Income Tax: The Revenue Act of 1861 levied a 3% flat rate income tax on those with an annual income at or exceeding $800 (equivalent to $24,100 in 2021). In 1861, only 3% of the population had an annual income of at least $800; as such, the tax enjoyed relatively widespread support among legislators. The act granted President Lincoln the power to appoint one principal assessor and one principal collector per state/territory; these officials were charged with enforcing income tax provisions. However, another portion of the bill stipulated that each state may collect and pay its own portion of the direct tax levied upon each state in its own way. Lacking an effective enforcement mechanism, the income tax provision was repealed in 1862 and replaced with a more expansive bill in the Revenue Act of 1862. The subsequent revenue act called for the establishment of the Internal Revenue Bureau (later renamed Internal Revenue Service) and a progressive tax scale.

A bond is a document of title for a loan. Bonds are issued, not only by businesses, but also by national, state or city governments, or other public bodies, or sometimes by individuals. Bonds are a loan to the company or other body. They are normally repayable within a stated period of time. Bonds earn interest at a fixed rate, which must usually be paid by the undertaking regardless of its financial results. A bondholder is a creditor of the undertaking.

Ebay ID: labarre_galleries